Preacher

Michael Saylor, the current CEO of Nasdaq-listed MicroStrategy, has become one of the most well-known preachers in the crypto community. In contrast to the erratic nature of Elon Musk, Michael Saylor is firm and relentless in his stance. For this reason, he has also gained a large number of followers in the crypto community.

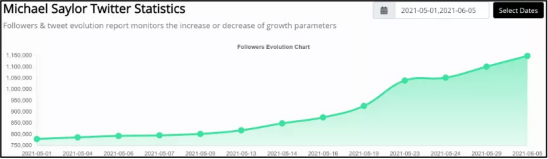

According to Speakrj, his Twitter followers have risen from 779,276 to 1,148,897 since May 1 alone, a cumulative increase of 369,021, or nearly 50%.

We know MicroStrategy is known for using large amounts of company cash and debt financing to buy bitcoin. The weight of its bets has made it the largest holder of long bitcoin positions on the public markets, so it's easy to understand why Michael Saylor himself is so keen on preaching bitcoin.

Betting History

MicroStrategy first disclosed its purchase and holding of bitcoin using the company's own cash on Aug 11th of last year, and has since made four additional investments, using a total of $500 million of its own funds to purchase 41,433 bitcoins at an average position cost of $11,947. On December 20th of last year and February 24th of this year, MicroStrategy issued convertible bonds to raise a total of $1.7 billion, purchasing 48,868 bitcoins at an average cost of $34,788.

Taken together, MicroStrategy used a total of $2.2 billion in funding to purchase 90,301 bitcoins at an average cost of $24,308 for the position. A single institution holding such a high position in bitcoin ranks first among all institutions that disclose relevant information. (Excluding cases like GBTC, which helps clients hold bitcoin on their behalf through a trust)

Since MicroStrategy first disclosed its bitcoin purchases, its shares have risen from $123.39 on Aug 20th all the way to a high of $1,315.00 and are currently down to $484.67. The highest gain was 961% and the current gain is 293%. The chart below shows that investing in Bitcoin has even turned MicroStrategy's stock into an extremely high volatility asset similar to Bitcoin.

Convertible Bond

We found that MicroStrategy used only $500 million of its own funds and $1.7 billion of debt financing, which is 3.4 times more than its own funds. Its debt financing is done through a financial instrument called convertible notes, specifically called Unsecured Senior Convertible Notes, which means the following:

l Unsecured: Unsecured bonds, which are liquidated after mortgage-backed bonds and before preferred shares.

l Senior: Senior bonds, liquidated after subprime mortgage-backed bonds and before subprime unsecured bonds.

l Convertible: Convertible bonds that can be exchanged for a certain percentage of the company's stock under certain conditions.

l Notes: Short-term bonds with a maturity of up to 10 years.

On December 7, 2020, MicroStrategy announced its first convertible bond program, a 5-year bond with a coupon rate of 0.75% and a conversion price of $398, a 37% premium to the then $289 share price. The bonds were initially planned to raise $400 million but eventually oversold for $650 million.

On February 15, 2021, MicroStrategy announced its second convertible bond program, a six-year bond with a 0% coupon and a conversion price of $1,432, a 50% premium to the then $955 share price. The bonds were ultimately scheduled to raise $600 million but ultimately oversold for $1.05 billion.

The convertible bond has three terms: redemption, repurchase, and conversion, which protect and limit the interests of both parties respectively. Since the bond is a private placement for institutional-type qualified investors without registration, the details are not disclosed and will not be elaborated in this article.

Structured Financial Instruments

Non-financiers may find it difficult to understand how low the interest rate is, even zero for the second issue. Zero-coupon bonds are actually very common in the market, but most zero-coupon bonds are issued at a discount. The bonds in this example are issued at par, mainly because the bondholders will receive conversion rights.

Analyzed from a financial engineering perspective, convertible bonds can be broken down into two parts: fixed-coupon bonds and call options. In the case of a secondary issue of convertible bonds, for example, the bond can be viewed as an investor purchasing a fixed-rate bond and then using all of the interest income from the fixed-rate bond to purchase a call option. An important component of the value of the option is the time value (i.e., the longer the term the higher the value), and since the option is a six-year option, the relative price is higher.

According to the data disclosure by cbonds, the investors of the two bond issues include the following. As you can see, all of its investors are convertible security-based ETFs, including First Trust, Bloomberg, and iShares' related ETFs. This could also explain why Bloomberg has been issuing frequent positive Bitcoin-related releases lately.

| Bonds | Investors |

|

650 Million Bonds | First Trust SSI Strategic Convertible Securities ETF |

| SPDR® Bloomberg Barclays Convertible Securities ETF | |

| iShares Convertible Bond ETF | |

|

1.05Billion Bonds | SPDR® Bloomberg Barclays Convertible Securities ETF |

| iShares Convertible Bond ETF |

Financial Analysis

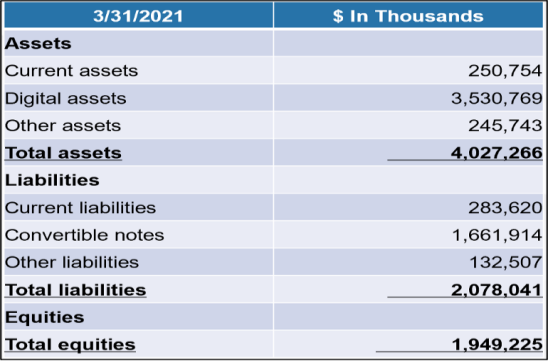

Nasdaq's disclosure statement accrues losses only for the "digital currency" asset class, not for the float. Therefore, a direct reading of MicroStrategy's 10Q statement for the first quarter can be very misleading. Based on the company's actual position, the summary balance sheet is as follows, after converting the price of $39,100 per BTC.

As you can see from the table above, MicroStrategy holds about $3.53 billion in bitcoin exposure. This compares to its net worth of $1.95 billion. Since the exposure to bitcoin is so large that it has little impact on its original primary business, we can think of the firm simply as a 1.81x leveraged hedge fund that is long bitcoin. If the price of bitcoin falls 55% to $17,500, the company will be insolvent.

At the current share price of $493, MicroStrategy has a market cap of $4.83 billion and a P/E ratio of 2.47x, which is too high a premium for a fund. And if you deduct the $1.2 billion market cap it had before it announced its bitcoin purchase, the increase in market cap for its bet on Bitcoin was $3.63 billion. The actual revenue generated by its bitcoin bet is only $1.34 billion at a coin price of $39,100, making the stock equally overvalued in relative terms.

The Crazy Gambler

Michael Saylor himself has a notorious history. An article written in June 2001 listed him as the biggest loser during the entire Internet bubble. At the time, MicroStrategy's stock rose from $120 to over $3,000 in just a few months, and Michael Saylor's reputation grew. The SEC even launched a massive investigation and charged him with misrepresenting the company's position.

In Summary

In the crypto community, retail investors who long bitcoin in the leveraged areas of exchanges pay an interest rate of about 36% annualized. And the annualized interest rate for borrowing USDT over-the-counter by pledging bitcoin is also generally above 12%. And both of these leveraged instruments create the risk of a blowout in the event of a cryptocurrency price crash.

It must be said that MicroStrategy has bridged the gap between the crypto and traditional worlds by using convertible bonds as a financial instrument to obtain negligible cost capital from the traditional world to bet on "high risk" crypto assets. And because of its clever design, it theoretically avoids the risk of blowing up. This is indeed a very smart strategy. However, it is probably because of the safety of the strategy itself that the positions have risen to such an exaggerated level. This is also in line with the usual ultra-gambling nature of the man Michael Saylor. It is difficult to quantify his actual risk tolerance as we do not have access to the details of the "mandatory repurchase" clause in his convertible bonds. We'll have to wait and see how it ends up.